Assessing granular real estate credit risk with Big Data analytics

In a short period of time private debt investments have become a favourite go-to allocation option both as a structural market opportunity and as an attractive source of yield returns. Over the past few years these two aspects have taken both managers and investors into increasingly more specialized and more granular lending strategies as previously targeted market segments have continued to re-price into lower expected return ranges and risk profiles have migrated as lending practices have been gradually relaxed to stay competitive.

In the case of private real estate debt allocations, the strategies have gone from replacing traditional bank financing for institutional quality income producing assets, a market opportunity created mainly due to post-GFC constraints in the banking system, to increasingly value-add capital driven opportunities and more recently into more granular lending targeting smaller assets and traditionally less institutional but potentially attractive market segments.

These developments have taken debt allocations into increasingly more specialized segments, managers, operational processes and execution that institutional investors have not previously been exposed to. Equally importantly as these market segments operate in highly fragmented ways, allocation decisions become relatively more reliant on less standardized data sources, limited information and analytical coverage. Investors of course rely on detailed information, consistent market data and objective risk assessment to make informed investment decisions and to manage risks on an ongoing basis.

One such niche area of real estate debt that is attracting institutional capital is residential bridge and development finance, where typically loans are advanced for relatively short periods of 1 to 3 years at up to ca 75% of a property’s market value. These strategies offer potential for attractive returns as well as other secondary benefits that institutional investors consider increasingly important. The strategies operate in the granular and less crowded market segment, loans are backed by real assets and typically have strong security package. In addition, other than the purely financial aspects there are also less immediately obvious but long term important positive non-financial aspects. Residential bridge and development finance plays an important role in the ongoing upgrading of the general housing stock and through this channel provides secondary and well-known socioeconomic benefits and environmental benefits such as upgraded technical standards and increased energy efficiency of the assets.

Ease of allocation options does not make up for lack of information

In order to allow investors flexible access to this specialized segment a number of allocation options have emerged in the past couple of years ranging from traditional closed-end funds to now also include listed bond exposures and most recently through shares in listed companies. Some of these options are also structured with additional financial leverage through loan-on-loan financing.

However, more flexibility in executing allocations does little to improve investor’s ability to objectively assess and quantify risks of these exposures. The newly established vehicles do not provide historical portfolio performance data, for obvious reasons as no such history exists for the specific offering. Lack of transparent data on both aggregate market performance and the performance of individual managers means that investors are faced with a level of analytical complexity in evaluating expected risk-adjusted returns and being able to objectively compare these strategies to other available options. In practice investors are predominantly relying on qualitative assessments of managers’ processes and operational capabilities such as origination and loan servicing but typically, qualitative factors alone are less than optimal to guide portfolio composition, allocation decisions and to objectively quantify the impact of various possible outcomes. Reliance on predominantly qualitative factors may expose investors to unexpected outcomes particularly when market conditions become less stable.

In order to make robust investment decisions investors need to quantify at least vital risk metrics such as PD (Probability of Default), LGD (Loss Given Default), EAD (Exposure at Default) and be able to model scenario outcomes and sensitivities to different adverse market conditions.

New data sources and big data analytics

New data sources and big data analytics can close the information gap for these new and increasingly important allocations through specific risk and rating methodologies. Implementing these new tools and technology can provide vital quantifiable risk metrics and profiles, can improve decision making processes at the outset and provide near real-time risk management tools for ongoing portfolio monitoring. With increased transparency institutional capital into these strategies could potentially increase at a faster rate and make bigger impact to the general housing stock. Managers too can benefit from these new tools to guide their own investment process in a more systematic way allowing them to allocate capital more efficiently as they navigate macro and micro market dynamics.

Kania Advisors is in the process of launching quantitative rating and risk assessment tools using big data and technology, which will provide an independent and systematically consistent view of risk profiles in bridge and development finance loans. The ratings will cover exposures ranging from individual loans to entire loan portfolios with the ability to monitor profiles and any migration in risk profiles in near real-time. Given the short-term maturity of loans of 1-3 years, there is a high degree of portfolio turnover and near real-time evaluation of various risk dimensions becomes relatively more important compared to longer maturity loan portfolios. The tools will also allow investors and managers to independently quantify portfolio tail risks, default correlations and sensitivity to future economic scenarios and will help to close the transparency and analytical gap to allow for more efficient and robust allocation decisions.

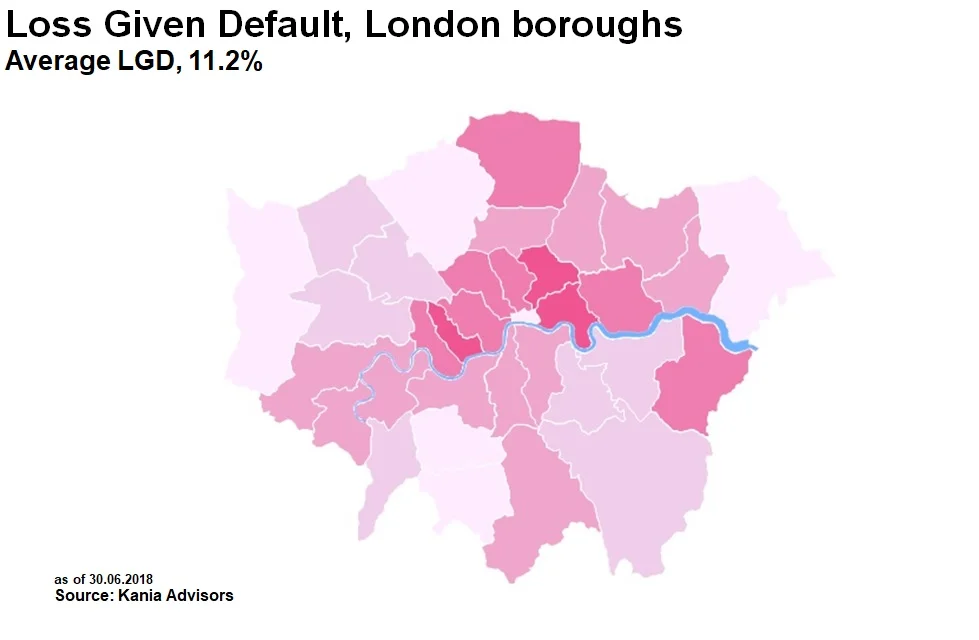

Below charts illustrate the Probability of Default and Loss Given Default for a standard loan with 75% loan-to-value across boroughs in Greater London.

For information about our services, please contact info@kaniaadvisors.com

About Kania Advisors

Kania Advisors is an independent research and advisory firm focused exclusively on institutional real estate allocations and investment programmes. We provide advice and solutions to improve outcomes in real estate investment programmes. We conduct detailed industry research and custom studies typically focused on quantitative analysis and provide insights which form a critical part of a client's decision process.